There are four CPA exam sections, or parts, including:

- Auditing & Attestation (AUD)

- Financial Accounting & Reporting (FAR)

- Regulation (REG)

- Business Environment & Concepts (BEC)

Essentially, each part of the Uniform examination is a 4-hour test covering a different subset of topics and concepts. Hence, in order to become a CPA, you must pass all four sections within an 18-month testing window with a score of 75 or higher.

- 1.Becker CPA Review Course: Rated the #1 Best CPA Review Course of 2024

- 2.Surgent CPA Prep Course: Best Technology

- 3.Gleim CPA Review Course: Largest Question Bank

You can take any section during an open testing window in any order you want. Furthermore, you are also allowed to take any number of exams in the same testing window. However, I wouldn’t recommend taking more than two in the same window. It’s too difficult to properly prepare for more than that at the same time. You don’t want to kill yourself. It is possible to sign up and take all four in one window, though.

You cannot, however, take a single section twice. Thus, if you fail one part, you will not be able to retake it until the next open testing window.

The AICPA is the body in charge of writing and creating the exam, but they aren’t in charge of administering it. Instead, each state administers the exam, reports scores to the candidates, and grants licenses to those of us who pass.

Let’s look at how the CPA exam is formatted, structured, and scored.

CPA Exam Sections Structure and Format

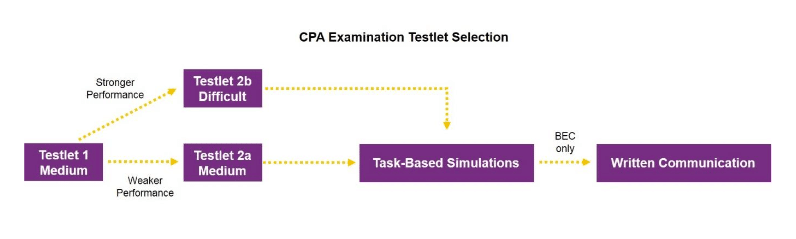

Each exam part is formatted into question blocks called testlets. These testlets contain either multiple-choice questions or task-based simulations. Additionally, each test starts out with several MCQ testlets followed by several Task-Based Simulation (TBS) testlets.

Multiple-Choice Question Testlets

Multiple-choice questions vary in difficulty and change as you correctly or incorrectly answer questions. For instance, each exam section starts with a medium difficulty MCQ testlet. Consequently, if you perform well on this testlet, you will receive a more difficult MCQ testlet on your second one. If you do well on this difficult testlet, you will receive an even more difficult group of questions on your third one. However, the opposite is true if you perform poorly on any testlet. Here’s what it looks like:

You might think, “Oh, this is good. I can make my exam easier by performing poorly on the first set of questions.” Wrong. You actually want more difficult questions because they are weighted more. Basically, one correctly answered difficult question will do more for your overall score than multiple correctly answered easy questions. Therefore, you are way better off answering difficult questions.

Hidden amongst the operational questions are pretest questions. These are questions that the AICPA is currently testing to see if they should include them on future exams. They are indistinguishable from normal testing questions and the answers will not affect your overall score.

Task-Based Simulation Testlets

Task-based simulations are problem set that allows you to apply your knowledge and demonstrate that you understand the topics on the exam. They are formatted differently on each exam part, but the most common formats include matching and fill-in-the-blank. Each part also includes one research question that requires you to research a topic in the authoritative literature and cite the code that discusses the current topic at hand. Most candidates feel these are more difficult than MCQs.

No two exams have the same number of questions and simulations, but you will have to navigate through each exam in a four-hour period. In prior years’ exams, each section had a different amount of time. Starting in 2017, the AICPA shortened FAR and added time to BEC, so all the sections had a 4-hour limit.

Written Communication Testlets

Also, BEC is the only one of the CPA exam sections with a written communication portion. Some candidates find this component easy, while others find it quite difficult. It’s pretty simple. They test your technical writing and communication skills by having you write a memo or client letter in a word processor. Your CPA review course should have a couple examples of this for you try and practice on.

Here’s how the CPA exam sections are all structured. This is a breakdown between multiple-choice questions and simulations on each section.

| Section | Multiple-Choice Questions | Task-Based Simulations | Written Communication |

|---|---|---|---|

| AUD | 72 | 8 | 0 |

| BEC | 62 | 4 | 3 |

| FAR | 66 | 8 | 0 |

| REG | 76 | 8 | 0 |

Get Discounts On CPA Review Courses!

Take $1,200 Off Surgent CPA Ultimate Pass

Get $1,140 Off Becker CPA Pro

Take $1,110 Off Surgent CPA Ultimate Pass

Enjoy $1,000 Off Gleim CPA Premium Pro

Becker CPA: 0% Interest Payment Plan

Becker CPA Advantage Package Now $2,499 – Promo

Get CPA Evolution Ready Content on All Becker CPA Courses

Take $1,500 Off Surgent CPA Ultimate Pass

Sale – Becker CPA Premium Package Now $3,099

Enjoy a 14-day Free Trial on Becker CPA Courses

Save on Becker CPA Single Part Courses

CPA Exam Scoring

The AICPA keeps changing the way they grade and weight the multiple-choice questions on the exam. It wasn’t that long ago that the questions were worth more than 70 percent of the total points on the test. That’s crazy. Each question was worth a ton.

In recent years, they have been backing off the value of MCQs and putting more importance on the task-based simulations. The MCQs are weighted evenly with the simulations except on BEC. Thus, the MCQs are only worth 50 percent of your points and the simulations are worth the other 50 percent.

Here’s a breakdown of how the CPA exam is graded and weighted.

| Section | Multiple-Choice Questions | Task-Based Simulations | Written Communication |

|---|---|---|---|

| AUD | 50% | 50% | 0 |

| BEC | 50% | 35% | 15% |

| FAR | 50% | 50% | 0 |

| REG | 50% | 50% | 0 |

CPA Exam Sections’ Content

Each of the four CPA exam sections encompass different broad topics that are broken down as follows:

Auditing (AUD)

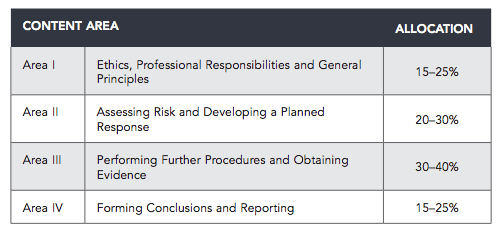

AUD covers all auditing and assurance services performed in public accounting. It tests your knowledge of the AICPA professional code of conduct, audit process, reviews, compilations, and attest engagements. Here’s a breakdown of what content is will appear on the exam.

- 15–25% – Professional Responsibilities, Ethics and General Principles

- 20–30% – Assessing Risk and Developing a Planned Response

- 30–40% – Performing Further Procedures and Obtaining Evidence

- 15–25% – Forming Conclusions and Reporting

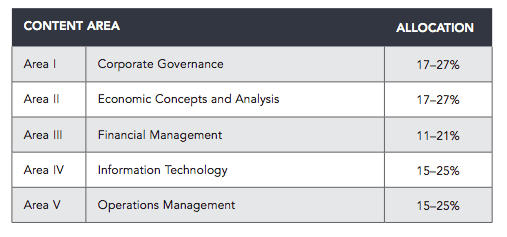

Business Environment and Concepts (BEC)

BEC is a comprehensive look at the environment that a business operates in. It covers topics like macro and microeconomics, cost accounting, management, and information systems. Here are the topics covered on BEC and what percentage they make up on the test.

- 17–27% – Corporate Governance

- 17–27% – Economic Concepts and Analysis

- 11–21% – Financial Management

- 15–25% – Information Technology

- 15–25% – Operations Management

Bonus: check out this great article covering all the best BEC study tips and most commonly missed topics!

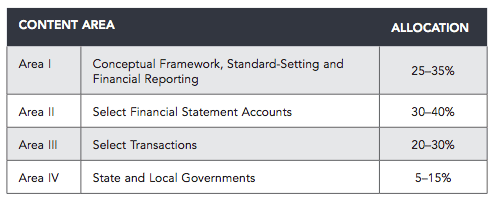

Financial Accounting and Reporting (FAR)

FAR covers the most information out of any exam section. It tackles the entire topics of financial accounting and reporting. This includes the FASB framework, financial statement preparation, US GAAP rules, and IFRS rules. Here is the content covered on FAR along with the percentages they make up on the exam.

- 25–35% – Standard-Setting, Conceptual Framework, and Financial Reporting

- 30–40% – Financial Statement Accounts

- 20–30% – Transactions

- 5–15% – Local and State Governments

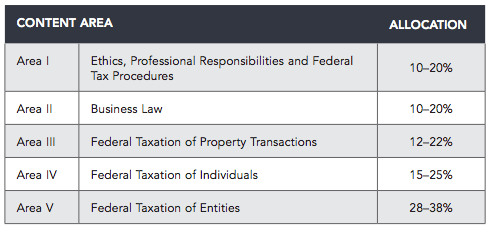

Regulation (REG)

REG is the only exam that doesn’t explicitly cover accounting topics. This section focuses on business and individual taxation, business law, and ethics. Here’s a breakdown on what is covered.

- 10–20% – Professional Responsibilities, Ethics, and Federal Tax Procedures

- 10–20% – Business Law

- 12–22% – Property Transaction Federal Taxation

- 15–25% – Individual Federal Taxation

- 28–38% – Entity Federal Taxation

Check out the best REG study tips!